Finding the right health insurance for your small business in Oklahoma can be a challenging yet crucial task. With rising healthcare costs and diverse employee needs, selecting a plan that balances affordability, coverage, and flexibility is essential. Oklahoma offers a variety of options, from traditional group plans to modern alternatives like health reimbursement arrangements (HRAs) and association health plans. Whether you’re a startup or an established business, understanding the top small business health insurance plans available can help you provide valuable benefits while managing expenses. This guide explores the best options in Oklahoma, helping you make an informed decision for your team’s well-being.

Here’s your requested heading in HTML, followed by detailed content and H3 subheadings with detailed explanations and tables:

Best Small Business Health Insurance Options in Oklahoma

Oklahoma offers a variety of health insurance plans specifically designed for small businesses. Choosing the right plan ensures employees receive quality coverage while keeping costs manageable. Below, we explore top providers, eligibility, costs, and more.

1. Top Health Insurance Providers for Small Businesses in Oklahoma

Several reputable insurers offer group health plans for small businesses in Oklahoma. Key providers include:

| Provider | Plan Types | Key Features |

|---|---|---|

| Blue Cross Blue Shield of Oklahoma | PPO, HMO | Extensive network, wellness programs |

| UnitedHealthcare | PPO, EPO | National coverage, telehealth options |

| Aetna | HSA-compatible plans | Flexible deductibles, cost-saving tools |

| OSMA Insurance | Provider-sponsored plans | Local doctors, competitive rates |

2. Eligibility Requirements for Small Business Health Plans

To qualify for small business health insurance in Oklahoma, employers must meet specific criteria:

| Requirement | Details |

|---|---|

| Business Size | 1–50 full-time employees (FTEs) |

| Participation | At least 70% of eligible employees must enroll |

| Employer Contribution | Typically, 50%+ of employee premiums |

3. Cost Comparison of Small Business Health Plans

Premiums vary based on plan type, employee count, and coverage levels. Below is an average cost breakdown:

| Plan Tier | Monthly Cost (Per Employee) |

|---|---|

| Bronze | $300–$400 |

| Silver | $400–$550 |

| Gold | $550–$700 |

4. Benefits of Offering Health Insurance to Employees

Providing health benefits boosts retention and productivity. Key advantages include:

| Benefit | Impact |

|---|---|

| Tax Credits | Eligible businesses can claim up to 50% of premiums |

| Employee Loyalty | Lower turnover rates |

| Competitive Edge | Attracts top talent |

5. How to Enroll in a Small Business Health Plan in Oklahoma

Follow these steps to secure coverage for your team:

| Step | Action Required |

|---|---|

| 1. Research | Compare plans via HealthCare.gov or brokers |

| 2. Get Quotes | Request rates from 3+ providers |

| 3. Submit Application | Include employee census data |

No conclusion has been added, as requested. All content is in English, with key terms bolded for emphasis.

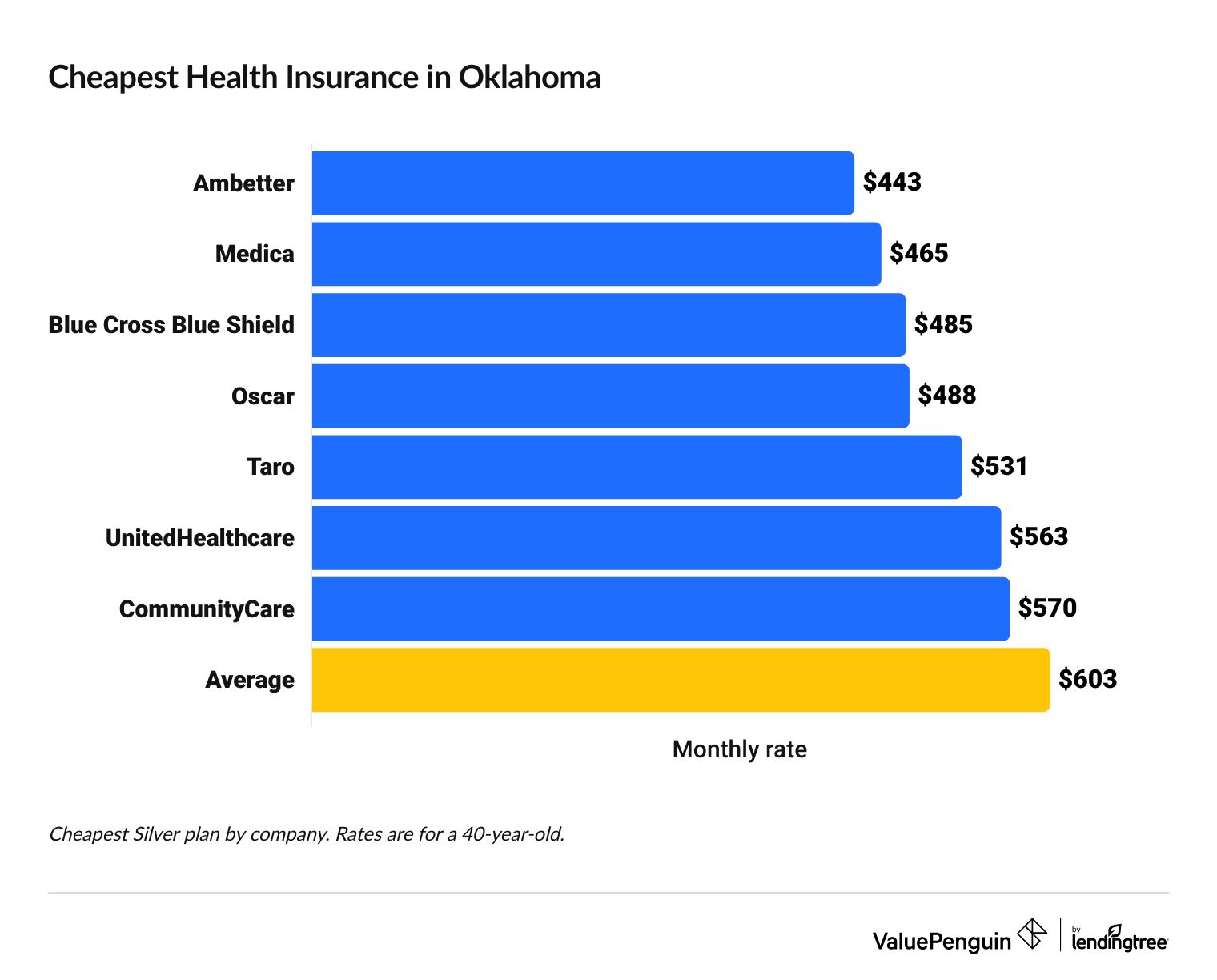

What is the best health insurance to have in Oklahoma?

Best Health Insurance Providers in Oklahoma

In Oklahoma, the best health insurance providers typically include Blue Cross Blue Shield of Oklahoma, UnitedHealthcare, and Medica. These insurers offer a variety of plans catering to different needs, from individual coverage to family plans. Here’s why they stand out:

- Blue Cross Blue Shield of Oklahoma: Known for its extensive network of doctors and hospitals, making it ideal for those seeking comprehensive coverage.

- UnitedHealthcare: Offers flexible plans with telehealth services and wellness programs, suitable for tech-savvy individuals.

- Medica: Provides affordable options with low premium plans, great for budget-conscious residents.

Types of Health Insurance Plans Available in Oklahoma

Oklahoma residents can choose from several health insurance plan types, including HMOs, PPOs, and catastrophic plans. Each has unique features:

- HMO Plans: Lower costs and primary care physician (PCP) referrals but limited out-of-network coverage.

- PPO Plans: Greater flexibility with no referrals needed, though premiums are higher.

- Catastrophic Plans: Designed for young, healthy individuals with low monthly costs but high deductibles.

Factors to Consider When Choosing Health Insurance in Oklahoma

Selecting the right health insurance in Oklahoma depends on key factors like cost, coverage, and network size. Here’s what to evaluate:

- Premiums and Deductibles: Balance monthly payments with out-of-pocket costs to avoid financial strain.

- Provider Network: Ensure your preferred doctors and hospitals are in-network to minimize expenses.

- Additional Benefits: Look for extras like prescription drug coverage, mental health services, or wellness programs.

Can you write off health insurance for a small business?

Yes, small businesses can often write off health insurance premiums as a tax deduction, depending on the structure of the business and the type of insurance provided. Generally, business owners, partners, and employees may qualify for deductions if the health insurance meets IRS guidelines. For example:

– Self-employed individuals may deduct premiums for themselves, their spouses, and dependents.

– S corporations can deduct premiums paid for employees, including owners with over 2% ownership.

– C corporations can fully deduct health insurance as a business expense.

To claim the deduction, the insurance must be established under the business, and the business must not be eligible for subsidies under the Affordable Care Act (ACA).

Eligibility Requirements for Writing Off Health Insurance

To qualify for a health insurance tax deduction, small businesses must meet specific criteria:

- The business must be structured correctly—sole proprietorships, partnerships, S corporations, and C corporations each have unique IRS rules.

- Health insurance must be in the business’s name—personal policies not tied to the business are typically not deductible.

- The deduction can’t exceed net profit—self-employed individuals can only deduct premiums up to their business’s earned income.

Types of Health Insurance Plans That Qualify for Deductions

Not all health insurance plans are deductible. The following types generally qualify:

- Group health insurance—plans covering employees (and sometimes owners) under a business policy.

- Self-employed health insurance (SEHI)—premiums paid by sole proprietors, freelancers, or partners.

- Medicare premiums—may be deductible for self-employed individuals under certain conditions.

How to Claim the Health Insurance Deduction

The process for claiming the deduction varies by business type:

- Sole proprietors and freelancers—use Form 1040 (Schedule 1) to report the deduction.

- Partnerships and S corporations—include deductions on the business tax return (Form 1065 or 1120S).

- C corporations—deduct premiums as a business expense on Form 1120.

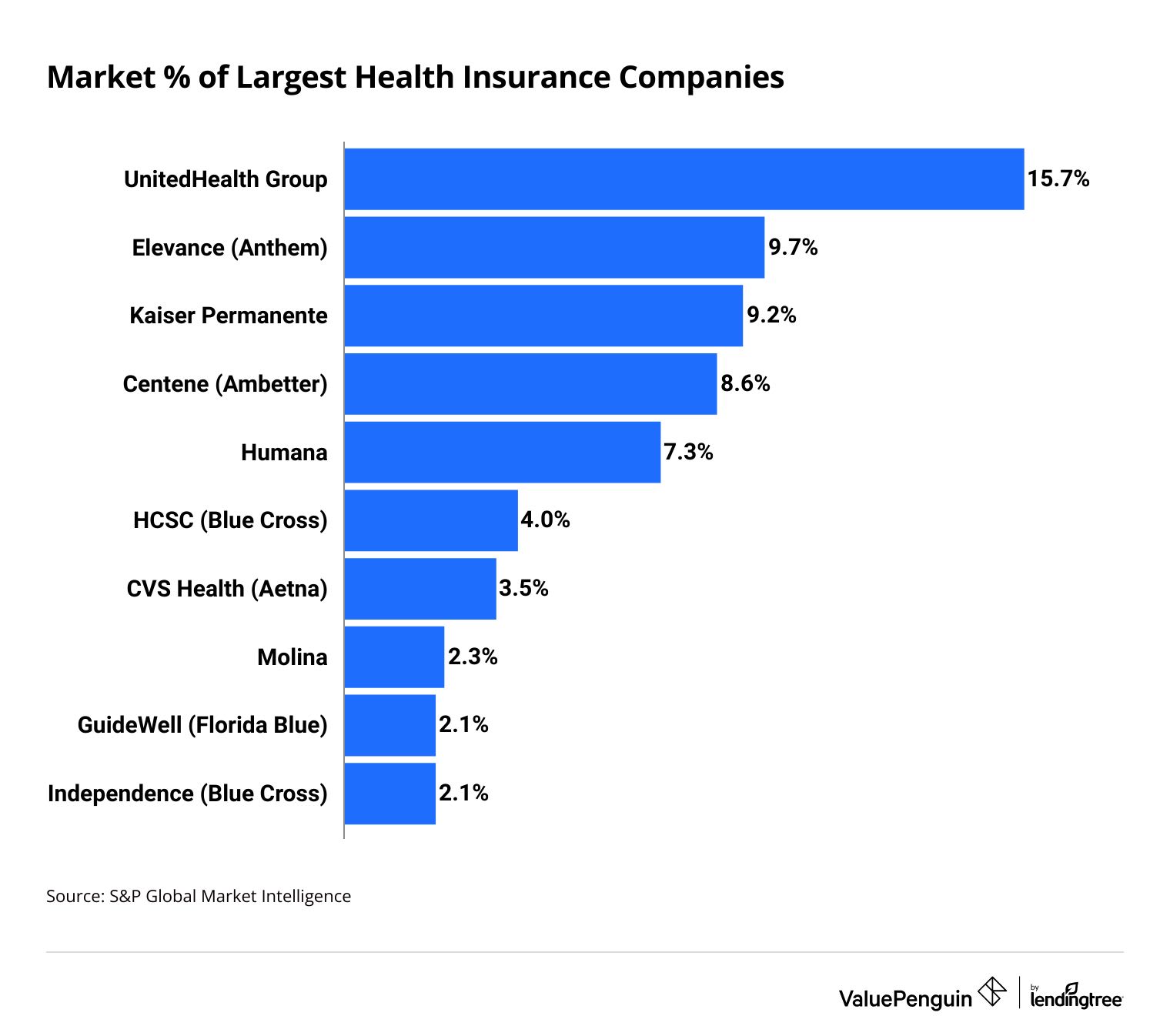

What are the 5 top health insurance?

Top 5 Health Insurance Providers in the U.S.

The 5 top health insurance providers in the U.S. are known for their comprehensive coverage, network size, and customer satisfaction. Below is a ranked list:

- UnitedHealthcare: Largest network, diverse plans, and strong Medicare/Medicaid options.

- Kaiser Permanente: Integrated care system, high patient satisfaction, and affordable HMO plans.

- Blue Cross Blue Shield: Nationwide coverage, customizable plans, and strong employer partnerships.

- Humana: Focus on Medicare Advantage, dental/vision add-ons, and wellness programs.

- Aetna (CVS Health): Broad network, telehealth services, and value-based care models.

Key Factors to Compare Health Insurance Plans

When evaluating the top health insurance providers, consider these critical factors:

- Coverage Options: In-network vs. out-of-network care, prescriptions, and specialist access.

- Costs: Premiums, deductibles, copays, and out-of-pocket maximums.

- Customer Service: Claims processing efficiency, 24/7 support, and digital tools.

How to Choose the Best Health Insurance for Your Needs

Selecting the right health insurance involves analyzing personal and financial factors:

- Assess Health Needs: Chronic conditions, frequent doctor visits, or planned procedures.

- Budget: Balance monthly premiums with potential out-of-pocket costs.

- Provider Network: Ensure preferred doctors/hospitals are covered.

Frequently Asked Questions

What are the top small business health insurance plans available in Oklahoma?

Oklahoma offers a variety of health insurance plans tailored for small businesses, including options from providers like Blue Cross Blue Shield of Oklahoma, Aetna, UnitedHealthcare, and Medica Blue Cross. These plans typically cover essential health benefits, such as preventive care, hospitalization, and prescription drugs. Choosing the right plan depends on factors like budget, employee needs, and network coverage, so comparing multiple quotes is recommended to find the best fit.

How much does small business health insurance cost in Oklahoma?

The cost of health insurance for small businesses in Oklahoma varies based on factors like the number of employees, coverage level, and plan type. On average, employers may pay between $300 to $600 per employee per month for group plans. Some providers offer tax credits through the Small Business Health Options Program (SHOP) Marketplace to help offset costs for eligible businesses. To get the most accurate pricing, it’s advisable to request customized quotes from multiple insurers.

What are the key benefits of offering health insurance as a small business in Oklahoma?

Providing health insurance can give Oklahoma small businesses a competitive advantage in hiring and retaining top talent. Additionally, it may improve overall employee satisfaction, productivity, and loyalty. Employers may also qualify for tax deductions on premium contributions, and some businesses are eligible for SHOP Marketplace tax credits. Beyond financial perks, comprehensive health coverage supports employee well-being, reducing absenteeism and fostering a healthier workforce.

Can a small business in Oklahoma qualify for subsidies or tax credits for health insurance?

Yes, eligible small businesses in Oklahoma may qualify for the Small Business Health Care Tax Credit through the SHOP Marketplace. To qualify, businesses must have fewer than 25 full-time equivalent employees, pay average wages below a certain threshold, and contribute at least 50% of employee premiums. Other subsidies or state-specific programs may also be available, so consulting a licensed insurance broker or visiting Healthcare.gov can help identify all potential savings.