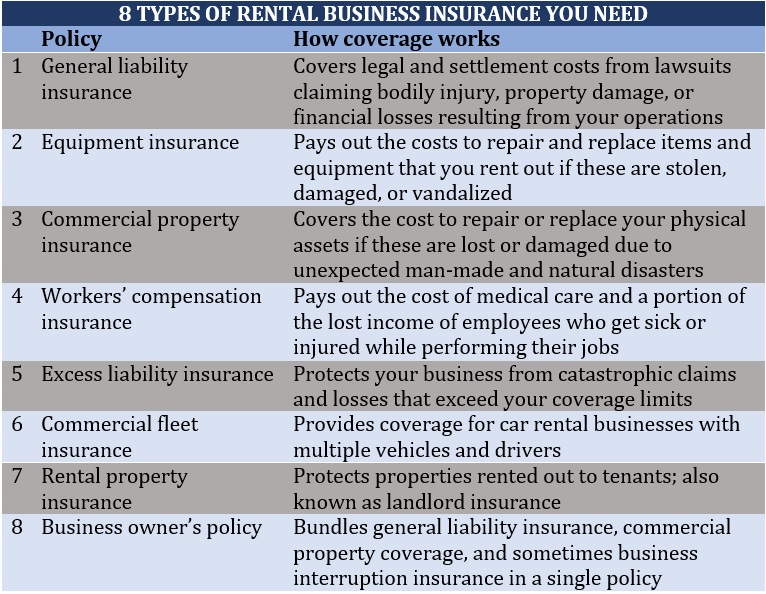

Running a party rental business comes with its share of risks—from property damage and accidents to unforeseen cancellations. Protecting your investment with the right insurance coverage is essential for long-term success. Whether you rent tents, tables, bounce houses, or audiovisual equipment, unexpected incidents can lead to costly liabilities. The right insurance policies not only safeguard your assets but also ensure peace of mind while serving clients. From general liability to equipment coverage, understanding your insurance options can make all the difference. This article explores the must-have insurance policies for your party rental business and how they can help you mitigate risks effectively.

Essential Insurance Policies for Protecting Your Party Rental Business

Running a party rental business involves managing valuable assets such as tents, tables, chairs, sound equipment, and more. Accidents, theft, or property damage can occur unexpectedly, making it crucial to have the right insurance coverage. Below, we explore the must-have insurance policies to safeguard your business from financial losses.

1. General Liability Insurance for Party Rentals

General Liability Insurance is a foundational policy for any party rental business. It covers third-party injuries, property damage, and legal fees if a customer sues your business. For example, if a guest slips on a wet dance floor you provided, this insurance would help cover medical expenses and potential legal costs.

| Coverage | Why It’s Important |

|---|---|

| Bodily Injury | Protects if a guest is harmed at an event |

| Property Damage | Covers accidental damage to client property |

| Legal Defense Costs | Pays for attorney fees in case of a lawsuit |

2. Commercial Property Insurance for Your Equipment

Commercial Property Insurance covers damage or loss to your rented equipment due to fire, theft, or weather. If a storm destroys your rented tents, this policy ensures you can replace or repair them without significant financial strain.

| Coverage | What’s Protected |

|---|---|

| Equipment Damage | Tents, tables, chairs, sound systems |

| Theft Protection | Covers stolen rental items |

| Natural Disasters | Storms, floods, or fire damage |

3. Inland Marine Insurance for Transported Goods

Inland Marine Insurance protects your equipment while it’s being transported. If a rental delivery van gets into an accident, this policy helps recover the cost of damaged or lost items.

| Coverage | When It Applies |

|---|---|

| Transit Protection | Covers goods in transit to events |

| Off-Site Coverage | Items stored at temporary locations |

| Accidental Damage | Vehicle collisions or mishaps |

4. Workers’ Compensation Insurance for Employees

If your party rental business has employees, Workers’ Compensation Insurance is legally required in most states. It covers medical bills and lost wages if an employee is injured while setting up or dismantling event equipment.

| Coverage | Benefits Provided |

|---|---|

| Medical Expenses | Doctor visits, surgeries, therapy |

| Disability Benefits | Income replacement during recovery |

| Legal Compliance | Avoids fines for non-compliance |

5. Event Cancellation Insurance for Business Stability

Event Cancellation Insurance reimburses lost income if an event is canceled due to unforeseen circumstances like extreme weather or vendor bankruptcy. This helps stabilize your cash flow and ensures financial recovery.

| Coverage | Applicable Scenarios |

|---|---|

| Weather Disruptions | Hurricanes, heavy rain, snow |

| Vendor Issues | Bankrupt or no-show partners |

| Non-Refundable Deposits | Recoups lost client payments |

How much is insurance for a party rental business?

What Factors Affect the Cost of Insurance for a Party Rental Business?

The cost of insurance for a party rental business depends on several factors, including the type of equipment rented, location, coverage limits, and the size of the business. Policies typically range from $500 to $3,000 per year, but high-risk items like inflatables or electrical equipment can increase premiums.

- Type of Equipment: Tents, tables, and chairs cost less to insure than bounce houses or audio systems.

- Location: Businesses in high-risk areas (e.g., cities with high theft rates) pay more.

- Coverage Limits: Higher liability limits or additional riders increase costs.

What Types of Insurance Are Needed for a Party Rental Business?

A party rental business typically requires multiple insurance policies to mitigate risks. General liability insurance is essential, but additional coverage like equipment insurance, commercial auto insurance, and workers’ compensation may be necessary.

- General Liability Insurance: Covers property damage or injuries caused by rented items.

- Commercial Property Insurance: Protects owned equipment from fire, theft, or vandalism.

- Event Cancellation Insurance: Safeguards against financial loss if an event is canceled.

How Can a Party Rental Business Save on Insurance Costs?

To reduce insurance expenses, a party rental business should compare quotes, implement safety measures, and adjust coverage based on risk. Bundling policies or increasing deductibles can also lower premiums.

- Shop Around: Compare quotes from multiple providers for the best rates.

- Safety Training: Proper staff training reduces accident risks and potential claims.

- Higher Deductibles: Opting for a higher deductible can lower annual premiums.

What insurance do I need for a rental business?

General Liability Insurance

General liability insurance is essential for any rental business as it protects against third-party claims for bodily injury, property damage, or personal injury. This coverage is particularly important if clients or visitors are frequently on your premises or using your rental equipment. Key aspects include:

- Bodily injury coverage: Protects if a customer gets injured while using your rental property or equipment.

- Property damage coverage: Covers damages caused by your rental items to someone else’s property.

- Legal defense costs: Helps cover legal expenses if your business is sued over a covered claim.

Property Insurance

Property insurance safeguards the physical assets of your rental business, including buildings, equipment, and inventory, from risks like fire, theft, or natural disasters. If your business relies on expensive tools, vehicles, or facilities, this insurance is critical. Important details include:

- Building coverage: Protects the structure of your rental property if you own the premises.

- Business personal property: Covers movable items like tools, furniture, or electronics used for rentals.

- Loss of income: Compensates for lost revenue if your property becomes unusable due to a covered peril.

Commercial Auto Insurance

If your rental business involves vehicles or you use company cars for deliveries, commercial auto insurance is necessary to cover accidents, theft, or liability. Standard personal auto policies won’t suffice for business-related vehicle use. Key components include:

- Liability coverage: Pays for injuries or damages your business vehicles cause to others.

- Collision and comprehensive: Covers repairs for your vehicles from accidents, vandalism, or natural disasters.

- Hired and non-owned auto coverage: Protects when employees use personal or rented vehicles for business purposes.

Can you legally run a business without insurance?

Is It Legal to Operate a Business Without Insurance?

The legality of running a business without insurance depends on the type of business, location, and local regulations. Some industries, such as construction or healthcare, require mandatory coverage (e.g., workers’ compensation or professional liability insurance). However, many small businesses can legally operate without insurance unless mandated by law or contractual agreements. Below are key considerations:

- Mandatory insurance: Certain states or countries require specific policies, like workers’ comp for employees or auto insurance for company vehicles.

- Industry-specific rules: Professions like doctors or contractors often face stricter insurance requirements.

- Penalties for non-compliance: Fines, lawsuits, or business license revocations may apply if insurance is legally required but absent.

Risks of Running a Business Without Insurance

While some businesses can legally skip insurance, doing so carries significant financial and operational risks. Without coverage, a single incident could jeopardize the company’s survival. Consider these potential consequences:

- Personal liability: Business owners may face out-of-pocket expenses for lawsuits, property damage, or medical claims.

- Contractual barriers: Clients or partners often require proof of insurance before signing agreements.

- Reputation damage: Uninsured businesses may struggle to attract customers or investors wary of unchecked risks.

Types of Insurance Recommended for Businesses

Even if not legally required, certain insurance policies are strongly advised to protect against unforeseen events. Here are the most common types:

- General liability insurance: Covers third-party injuries, property damage, or advertising-related lawsuits.

- Professional liability insurance: Shields against claims of negligence or errors in services (critical for consultants or advisors).

- Commercial property insurance: Protects physical assets like equipment or office space from fire, theft, or natural disasters.

What business does not require insurance?

Businesses That Typically Do Not Require Insurance

While most businesses benefit from some form of insurance, a few exceptions exist where coverage may not be legally or practically necessary. These include:

- Sole proprietorships with no employees or assets: If you operate alone and have minimal financial risk, general liability insurance may not be essential.

- Freelancers or gig workers with low-risk roles: Writers, artists, or consultants working from home may not need coverage if their work doesn’t pose liability risks.

- Hobby-based businesses without revenue: Casual ventures (e.g., selling handmade crafts occasionally) often don’t require formal insurance.

When Skipping Business Insurance Might Be Possible

Certain scenarios allow businesses to operate without insurance, though caution is advised:

- No legal requirements: Some states or industries don’t mandate coverage for very small or specific business types.

- Minimal client interaction: Online-only businesses with no physical products or services may face fewer risks.

- Self-insurance alternatives: Companies with substantial cash reserves might cover minor losses out-of-pocket.

Risks of Operating a Business Without Insurance

Even if insurance isn’t legally required, going uninsured carries significant risks:

- Financial vulnerability: A single lawsuit or accident could bankrupt an unprotected business.

- Lost opportunities: Clients or partners often require proof of insurance before collaboration.

- Personal liability: Owners may be personally sued if the business lacks protection.

Frequently Asked Questions

Why is general liability insurance essential for a party rental business?

General liability insurance is crucial for a party rental business because it provides protection against third-party claims for bodily injury, property damage, or personal injury. If a guest trips over rented equipment and gets injured, or if your rental items accidentally damage a client’s property, this coverage helps cover legal fees, medical expenses, and settlements. Without it, your business could face significant financial losses from lawsuits and claims.

What does equipment insurance cover for party rental businesses?

Equipment insurance safeguards your party rental inventory from risks such as theft, vandalism, or accidental damage. Since tents, tables, chairs, and audio-visual gear are expensive to replace, this policy ensures your valuable assets are protected. Whether items are lost during transport or damaged at an event, equipment insurance helps cover repair or replacement costs, minimizing downtime and financial strain.

Do I need commercial auto insurance for delivering party rentals?

Yes, if your business involves transporting rental items, commercial auto insurance is a must. Personal auto policies typically exclude coverage for business-related accidents, leaving you liable for damages. Commercial auto insurance covers collisions, theft, and liability while transporting equipment, ensuring your vehicles and cargo are protected. Without this, a single accident could result in costly out-of-pocket expenses.

How can workers’ compensation insurance benefit my party rental company?

Workers’ compensation insurance is vital if you have employees, as it covers medical bills and lost wages for work-related injuries or illnesses. From lifting heavy equipment to setting up event spaces, employees face physical risks daily. This coverage not only protects your staff but also shields your business from lawsuits related to workplace injuries, ensuring compliance with legal requirements in most states.